Executive Summary

Germany’s financial regulatory environment, led by BaFin (Federal Financial Supervisory

Authority), is entering a new era of proactive enforcement. After scandals like Wirecard,

BaFin’s 2026–2029 strategy emphasizes early risk detection, AML/KYC compliance,

operational resilience, and stronger data integrity across all financial institutions.

For banks, AML and KYC compliance can no longer be viewed as administrative tasks.

BaFin enforcement now targets not only money-laundering breaches but also structural

and technological weaknesses that create systemic risk.

Forward-looking institutions are adopting RegTech solutions and AML software to

modernize their AML transaction monitoring and KYC processes. By investing in KYC/

AML software and explainable data pipelines, banks can ensure compliance while

improving efficiency and customer trust.

This whitepaper provides a blueprint for transforming compliance under BaFin’s tougher

standards, covering governance, AML monitoring, and data-driven workflows that define

the next generation of RegTech-enabled banking.

Whitepaper Contents

| Chapter | Description |

|---|

| Chapter 1 (The Why): | BaFin’s Evolution

Overview of BaFin and its continued evolution as Germany’s chief regulatory body. |

| Chapter 2 (The What): | Case Studies in Modern Enforcement

Case studies detailing examples of modern enforcement and multi-million euro fines. |

| Chapter 3 (The Where): | BaFin’s Strategic Focus Areas

BaFin’s enforcement policies and the five key areas under the microscope. |

| Chapter 4 (The How): | The Blueprint for Modernization

The actionable blueprint for building a defensible, modern KYC/AML ecosystem. |

| About | We Build Products

How we translate this blueprint into reality for our clients. |

| Glossary & Disclaimer | Key acronyms and a legal disclaimer. |

Chapter 1 (The Why) BaFin’s Evolution : From Crisis to Systemic Control

This chapter details that transformation, moving from its origins in the post-Wirecard

reforms to its current use of Supervisory Technology (SupTech).

Understanding this evolution is critical because it provides the “why” behind the new

enforcement mandate. We will then connect this new strategy to the concrete, real-world examples of financial penalties and operational restrictions detailed in Chapter 2.

These case studies are not isolated incidents; they are the clear, tangible outcomes of

this new systemic control doctrine.

1.1 Post‑Wirecard Reform and BaFin’s New Strategy

BaFin’s enhanced assertiveness in supervising Germany’s financial sector is a direct

consequence of past crises. The collapse of Wirecard in 2020 exposed grave oversight

lapses, prompting leadership and legal reforms to give the supervisor “more bite,” with

new expertise and special task forces established under President Mark Branson [1].

Early signals indicated a tougher, more proactive regulatory environment: fines and

public measures against institutions ranging from fintechs to large incumbents signaled

that process and control weaknesses would draw supervisory attention.

By mid‑2025, BaFin formalized its forward‑looking posture in a strategic roadmap for

2026–2029. The plan orients supervision toward systemic risk prevention: strengthen

financial stability; identify problem institutions early and act swiftly; bolster operational

resilience; intensify the fight against financial crime and better integrate sustainability

and innovation into day‑to‑day supervision [2]. The trajectory is a more assertive,

data‑driven regulator mandated to safeguard market integrity and stability

1.2 SupTech and Data‑Driven Oversight

A cornerstone of BaFin’s evolution is the adoption of SupTech (Supervisory Technology),

to augment oversight. Objectives emphasize integrating internal and external data

(including market/media) to spot issues earlier; scaling modular, risk‑focused onsite

reviews; and monitoring cyber threat levels and IT/outsourcing interdependencies across

the sector [2].

BaFin also encourages the productive interplay of RegTech (at firms) and SupTech (at

the supervisor) to improve outcomes under the principle “same business, same risks,

same rules” [3]. In practice, that means timely, retrievable evidence of control design and

performance, especially in AML/CTF, supported by automation and analytics. This also

requires firms to retain human oversight and accountability, a fundamental requirement

in German supervision to prevent the diffusion of responsibility as digital processes

take hold.

Chapter 2 (The What) Case Studies in Modern Enforcement (2022–2025)

This chapter moves from strategy to the current reality (The What) of enforcement. The case studies and data below are not edge cases, they are the tangible proof of BaFin’s new enforcement doctrine in action. We have selected these specific examples, ranging from global incumbents like J.P. Morgan and Deutsche Bank to high-growth fintechs like N26 and Solaris, to demonstrate the new breadth of BaFin’s focus.

** Key Enforcement Actions (2024-2025) **

- J.P. Morgan AG: A €55m fine for IT governance and data integrity failures.

- N26 Bank AG: A €9.2m fine for systematically late suspicious transaction reports (STRs).

The Lesson: BaFin is now penalizing both deep IT system failures and procedural non-compliance.

The key violations reveal a clear pattern: the regulator is aggressively targeting systemic failures in governance, AML processes, and STR timeliness, not just overt fraud. These are the practical, multi-million euro lessons in what BaFin now considers non-negotiable.

2.1 J.P. Morgan (28 Oct 2025): A Sobering Reminder on Data Integrity

In a move that sent a clear signal to global banks, BaFin imposed a €55 million fine on J.P. Morgan’s German entity. While full details are still emerging, early reports indicate the penalty is not for a traditional AML lapse but for significant, systemic deficiencies in IT governance and data integrity related to regulatory reporting [10]. This action, which appears to be another major operational failure, powerfully reinforces BaFin’s new focus on the technological foundation of compliance (Pillar 4). It proves that even the most sophisticated institutions are under scrutiny if their underlying data and IT systems are not demonstrably robust and auditable.

2.2 Deutsche Bank (04 Mar 2025): A €23.05m Penalty for Systemic Failures

In February 2025, BaFin imposed €23.05 million on Deutsche Bank AG for organizational breaches under securities rules, lapses in required recording of client‑order communications, and delays in account switching obligations. The fine comprised ~€14.8m (derivatives sales controls), €4.6m (recording), and €3.65m (switching) [4]. The lesson: operational discipline is non‑negotiable.

2.3 N26 (21 May 2024): Fintech Growth Meets Compliance Growing Pains

N26’s trajectory shows that rapid expansion demands commensurate control maturity. In May 2024, BaFin fined N26 €9.2m for systematically late suspicious transaction reports

in 2022 [5]. Earlier growth limits and supervisory warnings underline that timeliness and throughput in AML reporting are core outcomes, not back‑office afterthoughts.

2.4 UmweltBank (Apr 2025): Governance and Internal Controls Under the Microscope

In April 2025, BaFin fined UmweltBank €520k for under‑resourcing its compliance function (2020–2023) and failing to provide a complete compliance report to management for 2021/22 [6]. In the same month, BaFin ordered another bank to remediate wide‑ranging deficiencies across AML, internal audit, and IT/outsourcing; appointed a special commissioner; increased own‑funds requirements; and imposed €432.5k in fines [3].

2.5 Other Notable Enforcement Actions

- Solaris SE (Mar 2024): BaFin fined Solaris €6.5m for systematically late STRs [7].

- Raisin Bank AG (Aug 2025): BaFin issued a remediation order for AML/CTF deficiencies [8].

- Ziraat Bank International AG (2021): supervisory restrictions and safeguards severely constrained core activities [9].

Accelerate innovation, while managing compliance and risk with the industry's leading specialist agency

Talk to Us

| Case Study | Before

The Challenge | After

The Solution & Results |

|---|

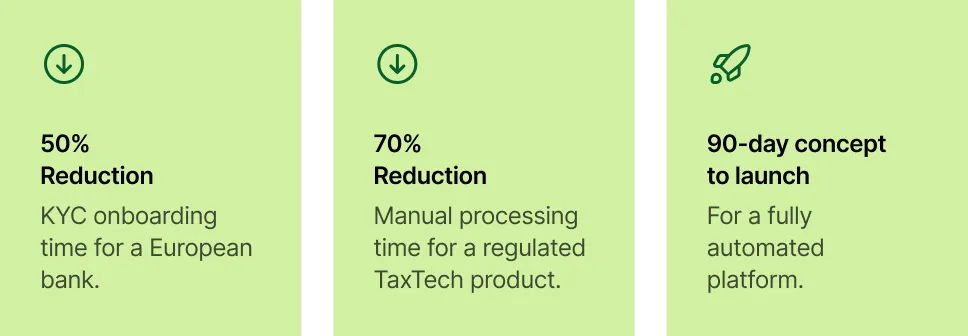

| European Bank Onboarding | Baseline: 45-day KYC process.

High customer drop-off.

Critical audit friction. | Intervention: Redesigned workflows & automated document extraction.

Outcome: 30% reduction in onboarding time & successful resolution of audit findings. |

| Greenfield Tax-Tech Platform (German Market) | Baseline: Manual, error-prone tax handling for German Freelancers, UGs, & GmbHs. | The Friction: No existing solution could handle the complexity of German tax logic automatically.

Intervention: Built two apps from scratch. Designed the product architecture and automated the full tax workflow for the German SME market.

Outcome: Concept-to-Launch in 90 days. Users can file for important documents from weeks and sometimes months to 3 business days. |

The principles in this paper are based on real-world implementation by our founding .

Chapter 3 (The Where) - BaFin’s Strategic Focus

If the first two chapters detail the regulator’s focuses and the “why” and “what,” this chapter explains the “where.” BaFin’s strategic focus areas are the specific domains where their new, proactive doctrine is being actively enforced.

These are high-priority areas that BaFin is actively examining during audits. The shift from simple checklists to enforcing substantive, data-driven controls is most evident here. Understanding these five areas from DORA’s IT resilience to the non-negotiable timeliness of STRs, is essential for building a modern and defensible compliance ecosystem.

The following five sections break down each of these high-priority domains in detail. Each one provides a practical analysis of how BaFin’s new expectations, moving from simple documentation to provable, data-driven resilience, are being applied in real-world audits. These are the specific rules of the new, non-negotiable compliance landscape.

3.1 IT Outsourcing and Third‑Party Risk (DORA)

This focus marks a fundamental shift from merely documenting vendor relationships to proving operational resilience against third-party failure. Under the EU’s Digital Operational Resilience Act (DORA) [10][11][2], vendor management is no longer a simple contract-review (SLA) task; it is a C-suite issue of business continuity.

Regulators are no longer just checking contracts. They are testing executable exit strategies and mapping concentration risk, for example, whether a bank is overly reliant on a single cloud provider for multiple critical functions. BaFin expects banks to maintain a dynamic, real-time outsourcing register (not a static PDF) and prove they can survive the sudden loss of a critical ICT provider without material disruption.

3.2 AML/CTF and STR Timeliness

The primary lesson from recent enforcement (e.g., N26, Solaris) is that timeliness is a non-negotiable outcome. BaFin’s ‘Risks in Focus 2025’ identifies inadequate money-laundering prevention as a critical risk [12]. The regulator is using hard metrics to measure the time taken from alert generation to filing the Suspicious TransactionReport (STR).

Banks are being forced to move beyond static, rule-based systems, which often generate excessive false positives, and into behavioral models that efficiently isolate true risk. Critically, this process must retain human accountability.

As Friedhelm Schmitt of Fincite cautioned at the 2025 Handelsblatt conference, ultimately “Die finale ENTSCHEIDUNG trifft der Mensch” (The final decision is made by the human) [20]. This means all automated systems must be transparent and support, not replace, the final judgment of a qualified analyst.

3.3 Internal Governance and Reporting (Compliance Culture)

This focus area concerns the structural integrity and top-down commitment to compliance. Recent fines (e.g., UmweltBank) highlight that inadequate resourcing, incomplete board reports, or reporting gaps are treated as severe failures of governance, not mere administrative oversights [2][11].

BaFin expects the management board to be proactively engaged, demanding clear, measurable KPIs (like compliance action closure rates) that signal the health of the control environment. This shifts board reporting from a retrospective explanation of what happened to a forward-looking risk management dashboard showing what is being done to prevent future breaches.

3.4 ESG and Sustainability Risks

BaFin expects Environmental, Social, and Governance (ESG) risks to be fully integrated into the bank’s core risk management framework (e.g., MaRisk), not treated as a peripheral marketing topic [13]. This means quantifying how climate change, transition risks, and social factors impact credit risk, operational resilience, and market positions.

For the compliance function, the emphasis is on evidential truthfulness. Claims of “green” or “sustainable” products must be substantiated with auditable data, preventing the legal and reputational risk of greenwashing and ensuring full compliance with disclosure rules.

3.5 Cybersecurity and Operational Resilience

This area focuses on proactive defense and rapid response. Cyber incidents are now treated as immediate prudential concerns [10][2][11]. Guided by BAIT (Bankaufsichtliche Anforderungen an die IT), BaFin expects banks to not only have detailed recovery plans (DR/BCP) but to rigorously test them and prove they can meet key metrics like Recovery Time Objective (RTO).

The introduction of DORA formalizes the need for rapid incident classification and timely notification to the regulator, turning every major cyber event into a critical compliance checkpoint. Banks must demonstrate architectural resilience (e.g., network segmentation, patch cadence) and incident readiness (e.g., playbooks, drills) to prove they are not a weak link in the financial system.

Chapter 4 (The How) The Bank Imperative: A Blueprint for Modernization

The previous chapters have established the new reality: BaFin’s strategic why(Chapter 1), the financial what of its enforcement (Chapter 2), and the specific where of its audit focus (Chapter 3). This final chapter answers the most important question: How does a bank build a compliance function that thrives in this new era?

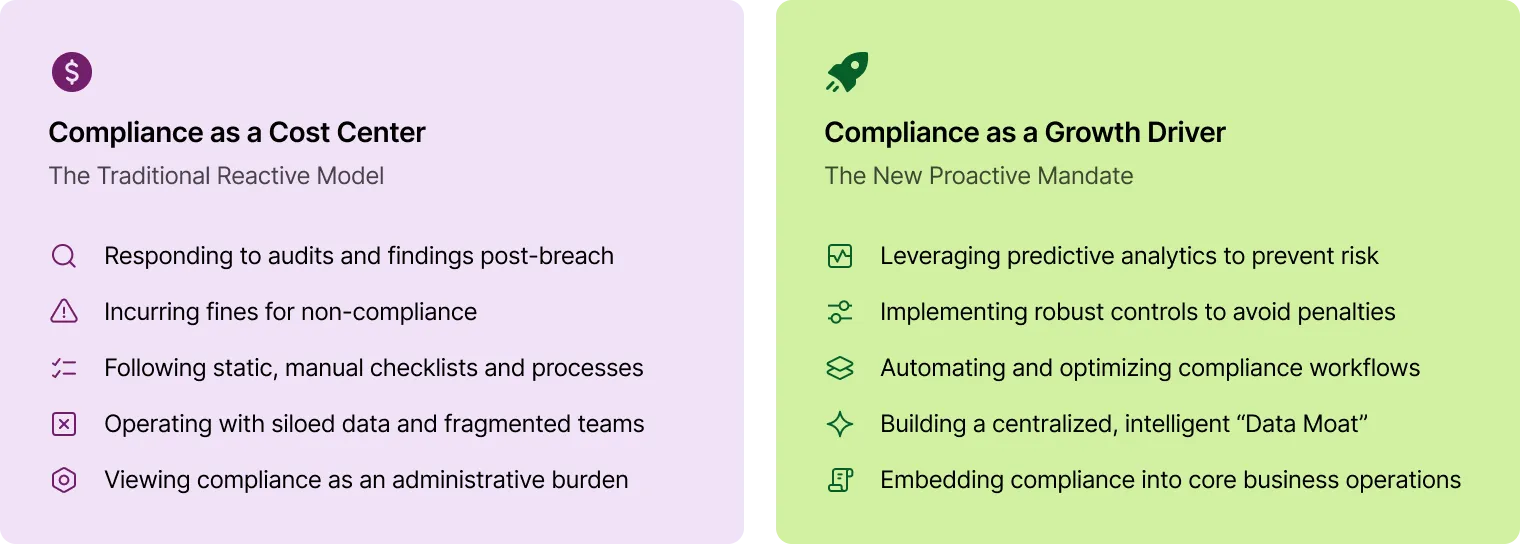

This is the actionable blueprint for modernization. It provides the framework for transforming compliance from a check-the-box cost center into a proactive, strategic capability. This blueprint is not simply a list of technologies; it begins with the critical human and process-oriented foundations in Pillar 0, which are the prerequisites for any successful technology implementation. The following pillars outline the path to building a defensible, efficient, and data-driven compliance function that satisfies regulators and creates lasting business value.

4.0 Pillar 0: Human-Centric Workflow Foundations

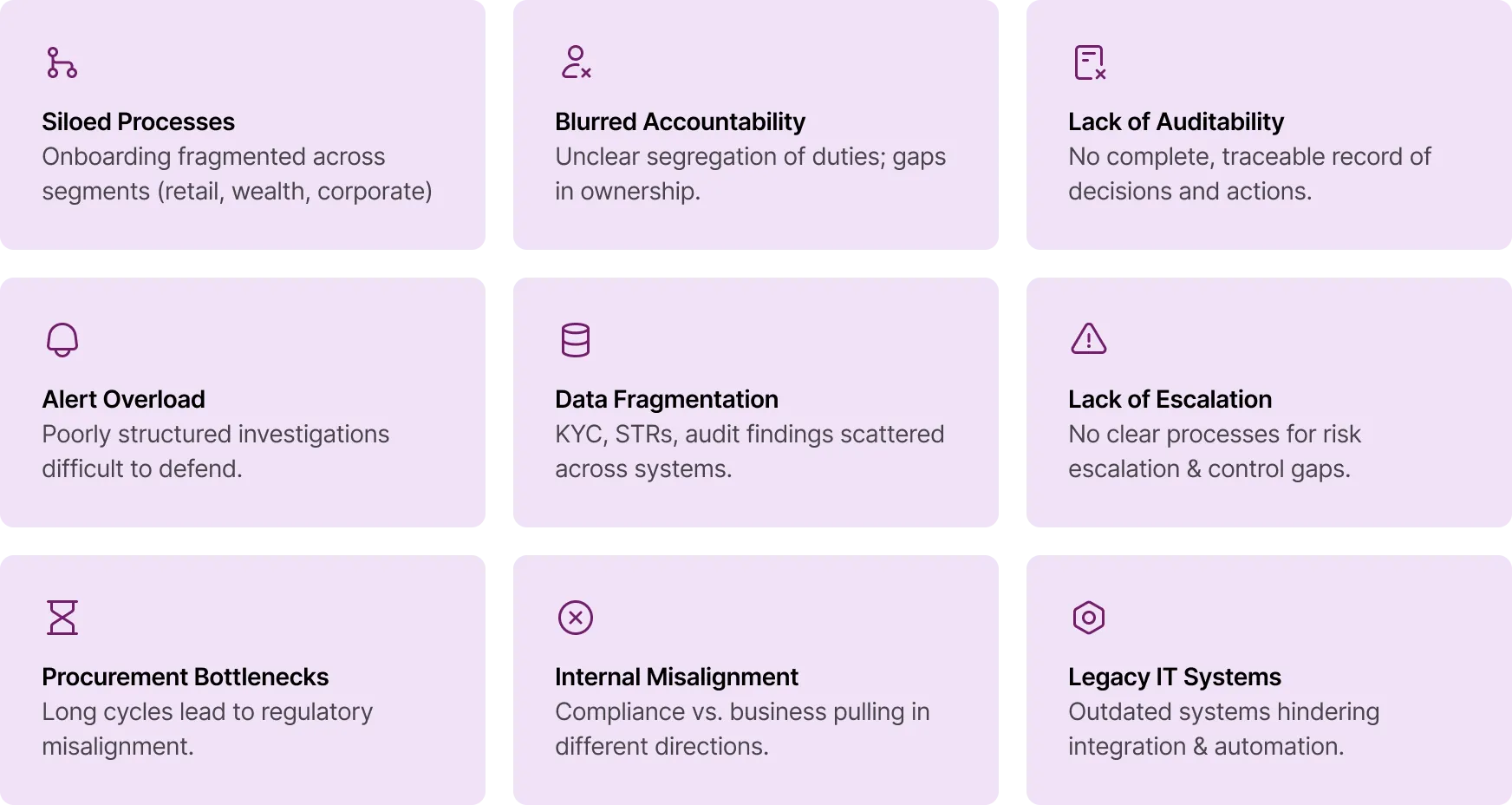

Achieving the transformative benefits of advanced regulatory technology (RegTech) is a complex challenge, extending beyond mere software adoption. Before financial institutions can fully leverage cutting-edge solutions, such as AI monitoring, machine learning for fraud detection, or sophisticated data analytics for risk assessment, they must first overhaul their internal operating models.

Banks must proactively address the deep-seated foundational workflow and organizational gaps that repeatedly undermine compliance efforts. These shortcomings include:

Designing Around the Core Stakeholders: Institutions that succeed orient their compliance processes around three stakeholder groups:

- Customers – Simple, transparent onboarding, with data collected once and re-used across products.

- Auditors and Supervisors – Complete audit trails “from day one,” with centralized, retrievable records that cut weeks of manual evidence-gathering.

- Internal Teams – Relief from manual drudgery, structured workflows that create accountability, and free analysts to focus on genuine risk.

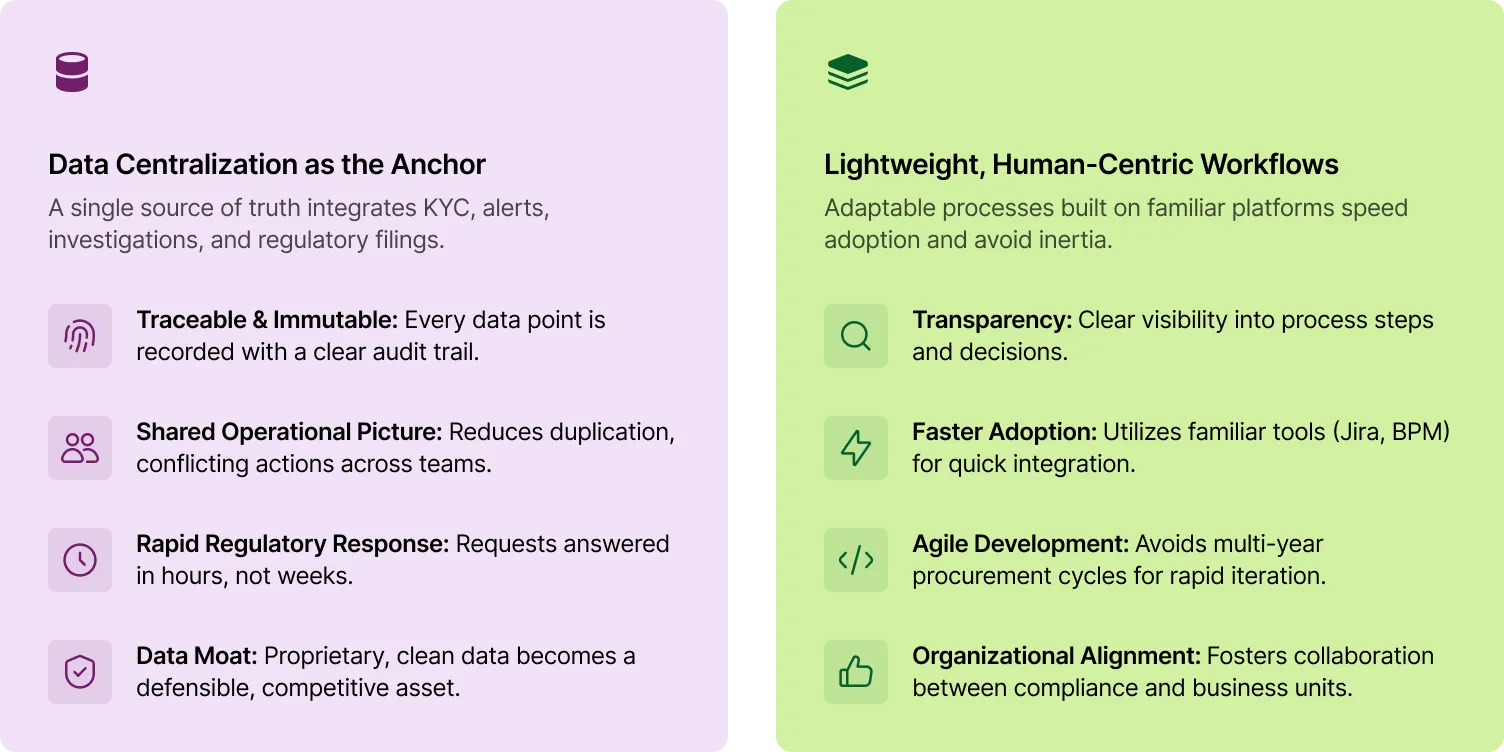

Data Centralization as the Anchor: At the heart of modern compliance is data centralization. Without a single source of truth, controls collapse under the weight of duplications, inconsistencies, and retrieval delays. A centralized case management system integrates KYC, alerts, investigations, and regulatory filings into one platform, ensuring that the centralized, clean, and proprietary data becomes the bank’s single most valuable asset. It is the Institutional IP, the “raw material” that, when fed into analytical models, creates the “Data Moat” discussed in Pillar 3. It is the one asset competitors cannot replicate.

Lightweight, Human-Centric Workflows: Many banks achieve more by adapting lightweight, human-centric workflows built on familiar platforms (e.g., Jira, Azure Board, BPM tools, workflow tools, RPA etc.). This creates transparency, speeds adoption, and avoids the inertia of multi-year procurement cycles.

By addressing these fundamentals first – workflow discipline, centralized data, and organizational alignment – banks lay the groundwork for Pillar 1 (Governance & Culture) and beyond. Without this “Pillar 0,” even the most sophisticated AI or monitoring system risks being undermined by silos, politics, and fragmented evidence.

The fix is to establish a clear transformation plan.

Talk to Us

A 3-Phase Transformation Roadmap

| Phase | |

|---|

| Phase 1: | Fix the Foundation (Months 1-3)

• Actions: Centralize Data, Map Workflows, Define KPIs.

• KPIs: STR cycle time baseline (e.g., 14 days), % alerts with full audit trail (e.g., 60%), % alerts with clear owners (e.g., 70%). |

| Phase 2: | Automate the Basics (Months 4-6)

• Actions: Implement Case Management, Automate Screening, Build Audit Trails.

• KPIs: False-positive rate ↓ (e.g., -20%), % alerts auto-enriched (e.g., 80%), % STRs auto-drafted (e.g., 50%). |

| Phase 3: | Build the Data Moat (Months 7-12)

• Actions: Deploy Behavioral Profiling, Enable Predictive Analytics, Tune Models.

• KPIs: True-positive rate ↑ (e.g., +30%), Time-to-triage ↓ (e.g., < 1 hr), Model drift < 5% per quarter. |

By addressing these fundamentals first, banks lay the groundwork for a scalable and defensible compliance function.

4.1 Pillar 1: Re‑engineered Governance and Culture

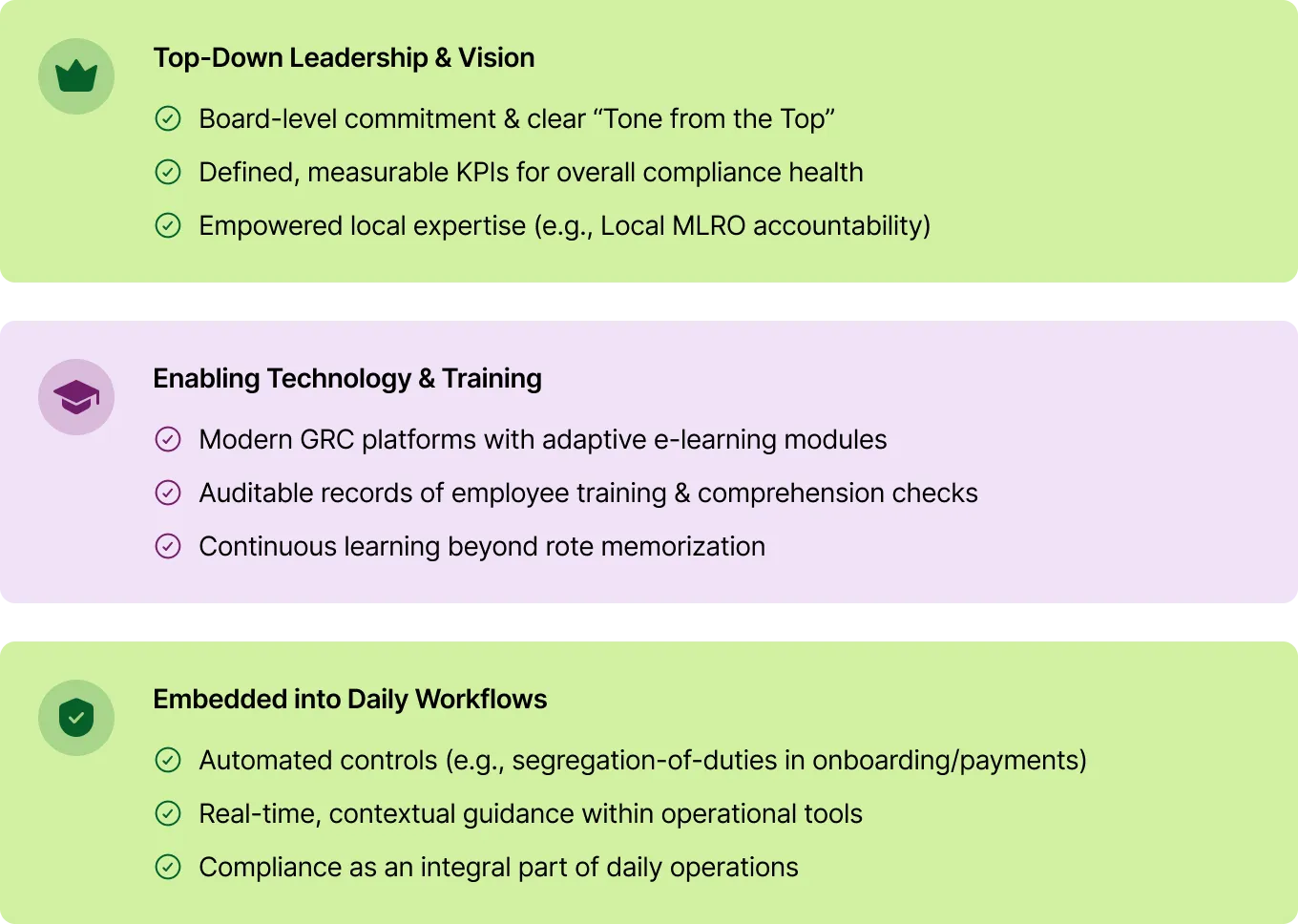

Establish a Local Center of Gravity: The complexity of German regulations (e.g., MaRisk, WpHG, GwG) and BaFin’s intensified supervisory approach demand a dedicated local expert. This person serves as a single point of accountability, can engage directly with the regulator on behalf of the MLRO and Deputy Function and is empowered to make decisions that reflect the unique risks of the German market. This dual reporting structure ensures that local compliance is not subordinate to global business targets, but has the authority to challenge and escalate when needed.

Implement a Proactive Oversight: A monthly, data-driven dashboard is the board’s new radar. Instead of waiting for a fine or a crisis to reveal a problem, this dashboard provides a real-time, holistic view of compliance health. It transforms compliance from an opaque back-office function into a measurable business metric. The board can track key indicators like STR timeliness and alert backlogs to identify potential issues before they become systemic failures.

This forward-looking approach enables timely interventions and demonstrates to BaFin that the bank’s leadership is actively engaged in risk management.

Cultivate a Compliance-First Culture: Compliance is not just the job of the compliance team; it is the responsibility of every employee. A compliance-first culture is built through top-down leadership and bottom-up engagement. This is supported by modern GRC (Governance, Risk, and Compliance) platforms and e-learning tools that provide adaptive training modules and comprehension checks.

By embedding segregation-of-duties and other controls directly into workflows like onboarding and payment approvals, the institution makes compliance an integral part of daily operations, reducing the risk of human error and demonstrating a robust, firm-wide commitment to integrity. This ensures a respected control environment.

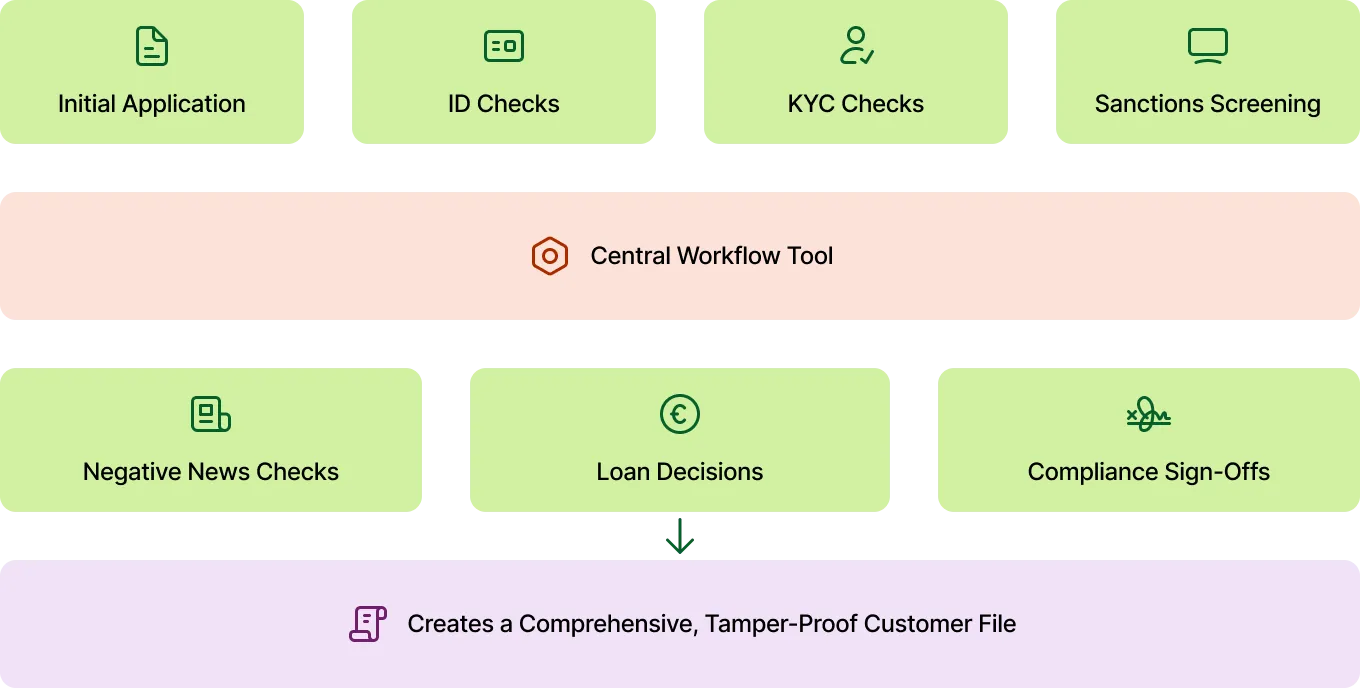

4.2 Pillar 2: Optimized Onboarding and Customer Vetting

Integrated Workflow and Centralized Data: The core of a modernized onboarding system is a central workflow tool. This tool acts as the “command center,” managing the entire customer journey from initial application to final approval. It ensures that all stakeholder actions, from KYC checks and loan decisions to

compliance sign-offs, are performed in a logical sequence and meticulously recorded. This not only standardizes the process but also eliminates data silos, ensuring a single, clean source of data for each customer segment. Data is collected and stored with an immutable audit history, creating a “customer file” that is comprehensive and tamper-proof.

Auditability and the “Right to Be Seen”: BaFin’s focus on structural and procedural weaknesses means banks must be able to demonstrate control over their processes. A modern system is designed with auditability in mind from the very beginning. Every action, check and decision is logged with a clear timestamp and stakeholder identity. Automated checks, such as sanction and PEP screenings, are run via controlled pipelines, and the results are stored instantly alongside the customer file.

This “storehouse for auditability” provides a granular, end-to-end view of the process, satisfying regulatory demands for transparency and demonstrating to supervisors that controls are not just in place, but are working as intended.

This ties directly to supervisory requirements for explainability: as articulated by Fincite’s Friedhelm Schmitt, the principle is “Nachvollziehbarkeit: Black Box = No Go” (Traceability: Black Box = No Go) [20], underscoring that every algorithmic decision must come with a clear, defensible rationale, converting complex models into auditable processes.

An Adaptable Investigation Framework: Finally, a modern system includes an adaptive investigation framework. When a red flag is raised, either by a human or an automated system, the framework provides a structured workflow for investigation, evidence gathering, and escalation. This ensures that every suspicious case is handled consistently and efficiently, and the data gathered during the investigation can be used to continuously train and improve the bank’s predictive models. This feedback loop makes the system smarter over time, a powerful demonstration of a forward-looking, prevention-oriented compliance function.

Enabling Intelligent Automation: Once this strong foundation is established, a bank can confidently deploy technology to streamline operations. Automation reduces manual effort and error in repetitive tasks like data verification and sanctions screening. With clean, well-structured data, the bank can then introduce AI and machine learning for more advanced tasks:

- Embedding AI-Driven Vetting: Automated checks can screen IDs, cross-reference data, and perform real-time sanction/PEP list screenings. Crucially, Explainable AI (XAI) ensures that every automated risk decision comes with a clear, defensible rationale, which is critical for supervisory review.

- Contextual Note on AI Adoption: The maturity of AI adoption varies significantly across the German banking sector. As highlighted in the 2025 Handelsblatt “AI in Banking” conference, many institutions are still moving from hype to strategic reality. While fintechs like SumUp are successfully deploying machine learning for real-time fraud detection and Generative AI to accelerate SAR narratives [22], larger established banks are often focusing initial AI efforts on internal efficiency, such as document processing, code development, and compliance reporting [23]. This reflects a “start in the back-office” approach [24] to manage AI’s ‘hallucination’ risk and build trust before deploying it in high-risk, customer-facing decisions.

- Behavioral Profiling for Risk Scoring: By analyzing a customer’s typical patterns (login, device usage, transaction types), the system can build a behavioral baseline. This allows for the flagging of subtle, “pre-crime” anomalies that static rules might miss, preventing issues before they become reportable. This can be used with varying degrees of success for fraud detection and monitoring.

- STR Workflows: The time between detecting a suspicious activity and filing a Suspicious Transaction Report (STR) is a critical performance metric for regulators. BaFin has publicly penalized institutions for systemic delays, signaling that timeliness is a non-negotiable compliance outcome.

A streamlined workflow that automates the final, critical steps of the process. Once a suspicious activity has been confirmed by an analyst, the system can automatically generate a pre-populated STR (Verdachtsmeldung) and route it for final review and submission. Case management timestamps embedded in the workflow provide an irrefutable, digital audit trail to evidence timeliness and demonstrate a clear commitment to prompt regulatory reporting.

4.3 Pillar 3: Autonomous Monitoring and Predictive Analytics

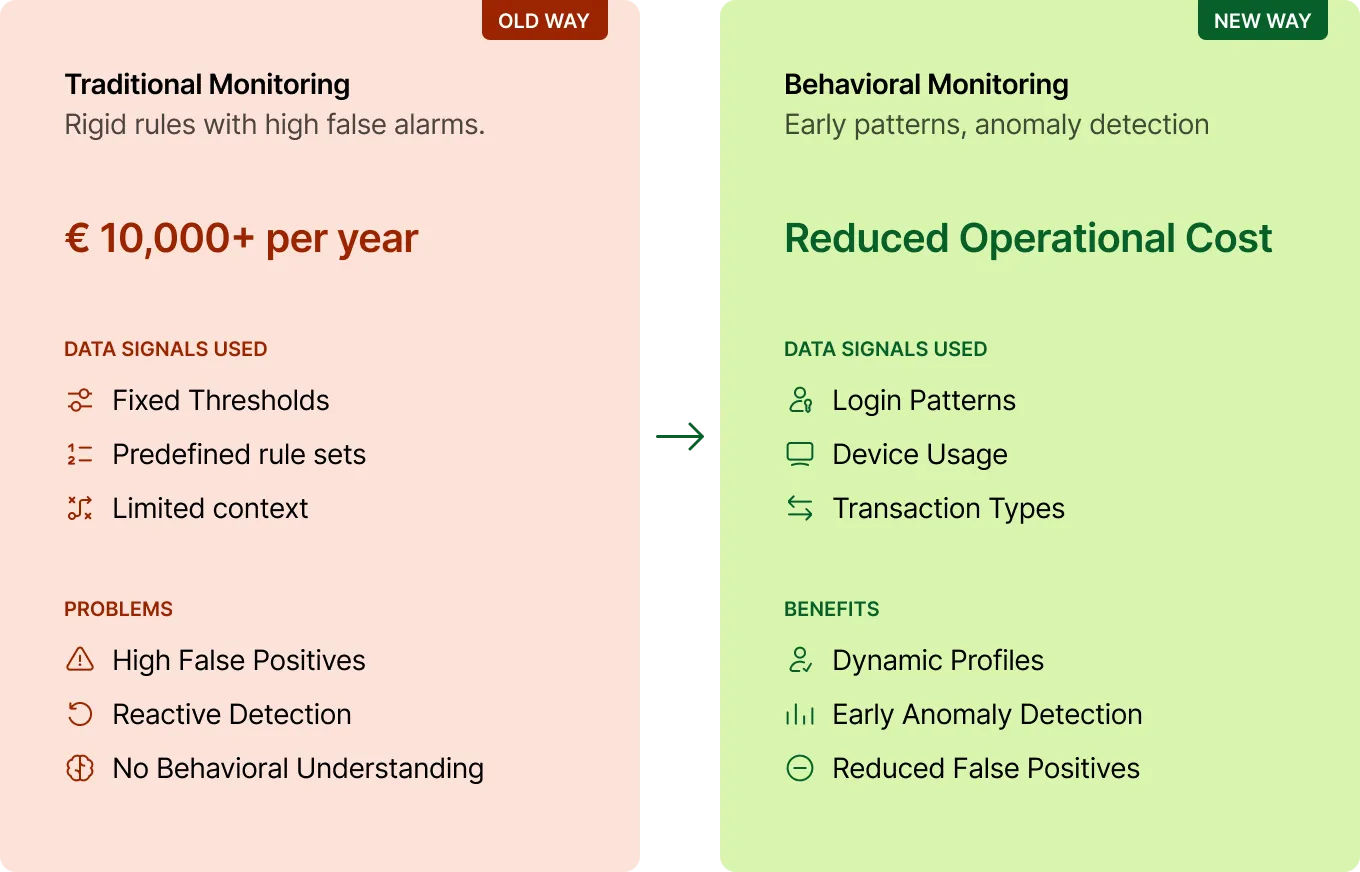

Behavioral AML Transaction Monitoring: The most significant weakness of traditional monitoring is its reliance on fixed thresholds (e.g., “flag any transaction over €10,000”). Today’s systems move beyond this by first establishing a unique, data-driven profile for each customer or customer segment.

The Data Moat in Action: Before vs. After

| Feature | Traditional AML System

High-Noise | Data Moat System

High-Fidelity |

|---|

| The Alert | ”Transaction > €10,000" | "New €10k transaction to a high-risk jurisdiction, breaking a 6-month behavioral pattern.” |

| The Result | 500+ alerts/day | 50 high-confidence alerts per day |

| The Outcome | 95% False Positives | 70% True Positives |

| The Risk | STR filed late

(BaFin violation) | STR auto-generated & filed in 24h |

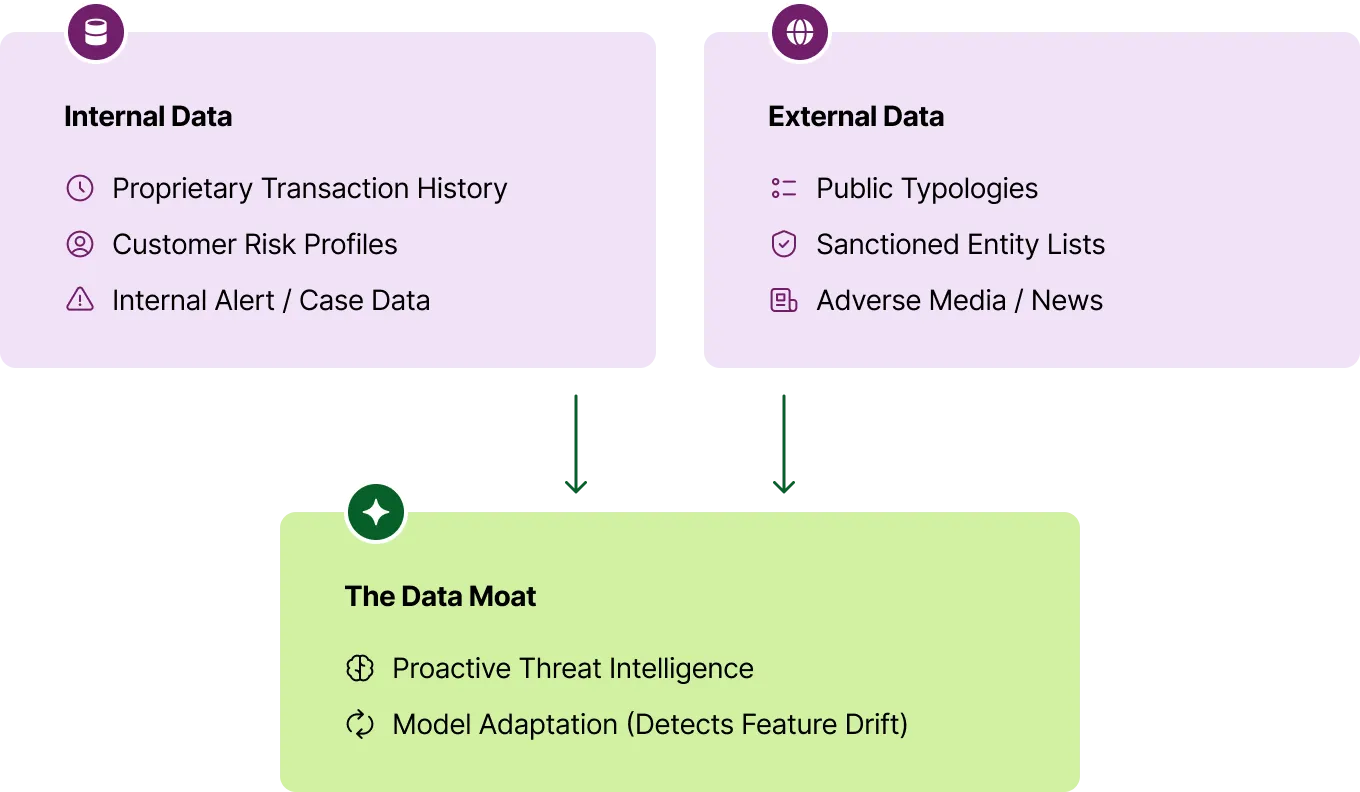

As Dr. Nicolas Flores Herr of Fraunhofer IAIS emphasizes, this “Datengraben” (Data Moat) is built by continuously feeding proprietary data through KI-Datenpipelines (AI Data Pipelines) [22]. This system can also ingest external data (public typologies, adverse media) to proactively adapt its models to new threats.

This baseline of “normal” behavior, from login patterns and device usage to typical transaction types and counterparties, allows the system to identify subtle anomalies that would otherwise be missed. By tuning and refreshing these behavioral models quarterly, the bank ensures its detection capabilities remain relevant and effective against emerging typologies, while also significantly reducing the burden of false positives.

Predictive Threat Intelligence: The foundation of Predictive Threat Intelligence is leveraging the bank’s proprietary data to create a “Data Moat.” As Dr. Nicolas Flores Herr of Fraunhofer IAIS emphasizes, this “Datengraben” (Data Moat) is built not just from volume, but by continuously feeding proprietary data through KI-Datenpipelines (AI Data Pipelines) to build a sustainable competitive and compliance advantage [21].

The most advanced compliance programs go beyond simply reacting to internal alerts; they integrate with the wider financial crime ecosystem. Predictive threat intelligence systems ingest data from external sources, including public typologies, sanctioned entity lists, and adverse media, to identify and forecast new threats. The system actively monitors for “feature drift” (when a criminal pattern changes) and automatically adapts its models.

By continuously tracking performance metrics like precision, recall, and false-positive rates, the bank can demonstrate to regulators that its controls are not static, but are constantly learning, improving, and staying ahead of the criminals. This proactive posture transforms compliance from a reactive obligation into a strategic function that safeguards the bank and the broader financial system.

4.4 Pillar 4: A DORA‑Ready IT & Data Ecosystem

BaFin and the ECB are now scrutinizing third-party relationships under the Digital Operational Resilience Act (DORA). This isn’t about just checking a box; it’s about managing systemic risk. A live outsourcing register isn’t just a document; it’s a dynamic tool that gives the bank real-time visibility into its supply chain vulnerabilities. By documenting executable exit plans, the bank can demonstrate its ability to maintain critical operations even if a provider fails, a key DORA requirement. This proactive management prevents a vendor’s failure from becoming the bank’s operational crisis.

Integrated Data Management: A single case platform for cyber security alerts as the source of truth eliminates fragmented data, a common cause of security failures. It allows for rapid, accurate data pulls for regulators, drastically shortening examination times and reducing supervisory friction. This holistic view of customer data across all systems also provides the foundation for advanced analytics and a deeper understanding of customer behavior.

Automated Regulatory Reporting: Manual reporting is prone to human error and is a major source of operational risk. Automated pipelines ensure data integrity and compliance with strict reporting deadlines set by standards like MiFID II/WpHG. Furthermore, ensuring data retention, immutability, and retrievability demonstrates a robust control environment, a cornerstone of BaFin’s expectations.

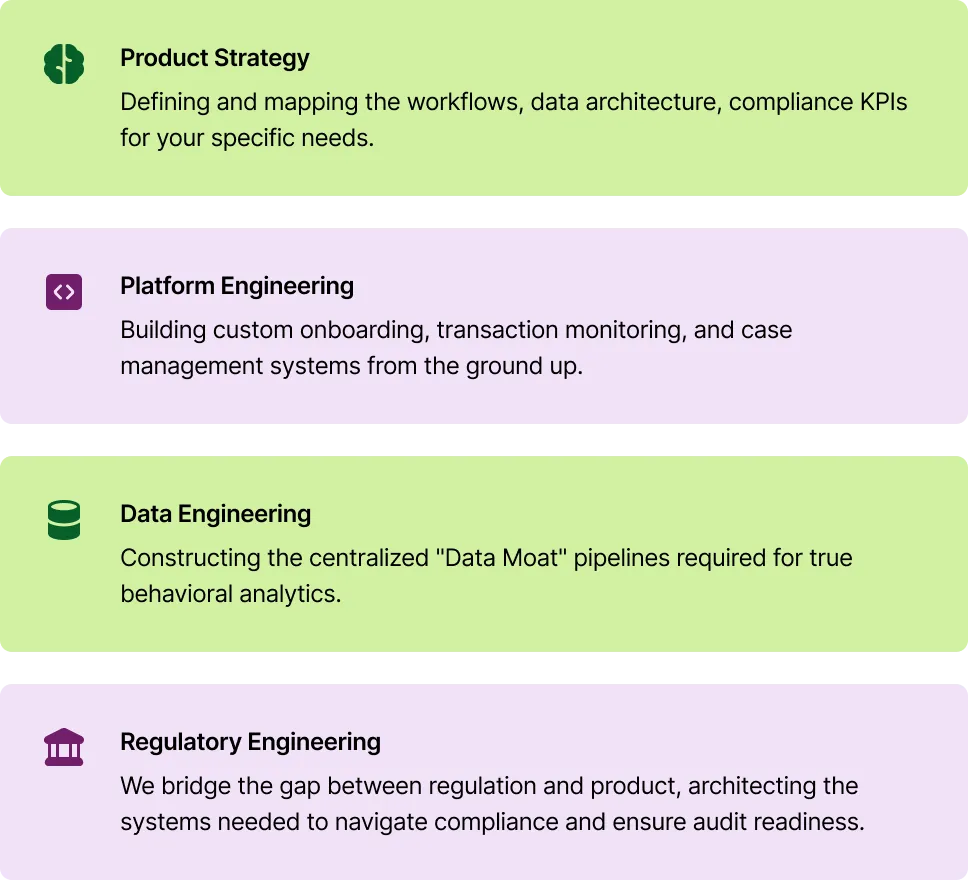

About We Build Products: Your RegTech Partner

We Build Products is a Berlin-based RegTech consultancy and product development firm. We specialize in building the high-performing AML/KYC platforms and data infrastructure required to thrive under BaFin’s new mandate. We translate the blueprint in this paper into reality.

Our Services

How we Work

Proof Points:

Who We Work With:

- Specialized Finance Leaders evolving into tech-enabled Fintechs.

- Traditional Players needing a technical partner to build custom, compliant platforms from scratch.

Chapter 5: Conclusion

The transformation of the German regulatory landscape is undeniable. BaFin has irrevocably shifted its focus from reactive auditing to proactive, systemic control. The central message of this whitepaper is that compliance can no longer be outsourced or treated as a siloed, back-office function; it must be the core operating model for sustainable growth.

The blueprint for modernization, from establishing a Human-Centric Workflow Foundation (Pillar 0) to implementing a DORA-Ready IT Ecosystem (Pillar 4), is the strategic roadmap for navigating this new era. This is not a theoretical model.

The pain points addressed and solutions proposed are forged from the author’s direct research and practical experience: sitting in high-stakes auditor meetings, demonstrating live onboarding and transaction monitoring workflows and engaging with the daily realities of MLROs, their deputies and regulatory consultants. This real-world foundation anchors the concept of the Data Moat: leveraging proprietary internal data and secure AI Data Pipelines (KI-Datenpipelines) to build detection systems that are not only highly effective but also fully explainable and auditable, meeting the core principle that “Nachvollziehbarkeit: Black Box = No Go.”

The cost of inaction is clear, demonstrated by the multi-million euro fines and stringent operational restrictions imposed on institutions large and small. Conversely, the reward for proactive compliance is competitive advantage: faster onboarding, massive efficiency gains through false-positive reduction, and enhanced brand trust.

By embracing RegTech (Regulatory Technology) and strategically deploying Machine learning, Artificial intelligence and structured data, German banks can move above and beyond compliance, securing their stability, improving their unit economics and positioning themselves as resilient leaders in the European financial ecosystem. The time to build this foundation is now.

About the Author

Mohan Paranthaman is a product and compliance leader with over 20 years of experience in product development and management. He has extensive expertise in RegTech, building solutions that balance growth with regulatory trust.

As Co-Founder and CPO of We Build Products, he applies a holistic approach to compliance and product strategy, drawing on his experience at institutions like Citi, BNP Paribas, and Akbank. His work includes the complete revamp and optimization of onboarding, KYC, and AML systems, demonstrating his ability to meet stringent regulatory needs while driving business efficiency.

Your Path to Proactive Compliance: Next Steps

Book a complimentary, confidential call. Leave with 3 prioritized gaps and a benchmark KPIs.

Book Assessment

Appendix – Selected, Verified BaFin Enforcement Actions (2024–2025)

| Institution | Fine/Measure | Key Violations | Source |

|---|

J.P. Morgan AG

28 Oct 2025 | €45m | IT governance & data integrity failures | [10] |

Deutsche Bank AG

04 Mar 2025 | €23.05m | WpHG organizational breaches; recording lapses; ZKG switching delays | [4] |

N26 Bank AG

21 May 2024 | €9.2m | Systematically late STRs (2022) | [5] |

Solaris SE

Mar 2024 | €6.5m | Systematically late STRs | [7] |

UmweltBank AG

Apr 2025 | €520k | Under-resourced compliance; incomplete board report | [6] |

Raisin Bank AG

Aug 2025 | Remediation order | AML/CTF deficiencies | [8] |

Glossary & Disclaimer

-

AML/CTF: Anti-Money Laundering / Countering the Financing of Terrorism

-

BaFin: Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht)

-

BAIT: Supervisory Requirements for IT in Financial Institutions (Bankaufsichtliche Anforderungen an die IT)

-

DORA: Digital Operational Resilience Act

-

MaRisk: Minimum Requirements for Risk Management (Mindestanforderungen an das Risikomanagement)

-

MLRO: Money Laundering Reporting Officer

-

STR: Suspicious Transaction Report (Verdachtsmeldung)

-

XAI: Explainable Artificial Intelligence

Disclaimer: This document is for informational purposes only and does not constitute legal, financial, or regulatory advice. All information is provided “as-is” without warranty. Consult with qualified legal or compliance professionals before making any decisions based on this content. Outcomes depend on client context; examples are illustrative; no guarantee of regulatory results without actual implementation basis.

Endnotes / References (public sources)

[1] Reuters. “Germany’s new finance watchdog vows further supervision reforms.” 13 Oct 2021.

Read article

[2] BaFin. “BaFin’s objectives 2026 to 2029.”

View BaFin objectives

[3] BaFin measures & orders (Akbank AG, 2025), summary reporting via: GRCReport.

Read GRC report

[4] BaFin. “Publication of measures , Deutsche Bank AG (04 Mar 2025).”

View BaFin publication

[5] Reuters. “German regulator fines N26 Bank over late money laundering reports.” 21 May 2024.

Read article

[6] BaFin. (UmweltBank AG , fine for compliance organization shortcomings). Official notice (2025-04).

[7] ICLG. Anti Money Laundering Laws and Regulations Report 2025 , Germany.

View ICLG report

[8] AML Intelligence. “German fintech Raisin addresses AML issues after BaFin remediation order.” 28 Aug 2025.

Read article

[9] BaFin. (Ziraat Bank International AG , restrictive measures and safeguards, 2021).

View BaFin publication

[10] BaFin. “BaFin imposes €45 million fine on J.P. Morgan AG for data reporting failures.” Official Notice (28 Oct 2025).

View BaFin notice

[11] EUR-Lex. “Digital Operational Resilience Act (DORA).”

View DORA regulation

[12] European Central Bank (SSM). “Supervisory priorities 2024–2026.”

View ECB priorities

[13] BaFin. “Risks in Focus 2025 , 5. Risks arising from inadequate money laundering prevention.”

View BaFin risk focus

[14] BaFin. “Risks in Focus 2025 , 2. Sustainability.”

View BaFin sustainability focus

[15] Backbase press. “Helps banks cut onboarding time by 80% & boost operational efficiencies by 30%.”

Read press release

[16] PwC. “Digital Trust Insights.”

View PwC insights

[18] Cube Global / Banking Dive.

View compliance report

[19] ECB / BaFin.

View ECB priorities

View BaFin risk focus

[20] McKinsey / FTI Technology. (Compliance as competitive advantage).

View McKinsey insights

[21] Schmitt, Friedhelm (Fincite). Handelsblatt Conference 2025 (on Accountability and Auditability). Source reference: 09Schmitt.pdf

_Note: Full agenda and retrospective available via Handelsblatt Live

[22] Flores Herr, Dr. Nicolas (Fraunhofer IAIS). Handelsblatt Conference 2025 (on Data Moat and KI-Datenpipelines). Source reference: 01Flores-Herr.pdf

_Note: Full agenda and retrospective available via Handelsblatt Live

[23] Kant, Elisabeth (SumUp). Handelsblatt Conference 2025 (on practical ML/GenAI use cases). Source reference: 07Kant.pdf

_Note: Full agenda and retrospective available via Handelsblatt Live

[24] Paxmann, Stephan (LBBW). Handelsblatt Conference 2025 (on AI in payments and operations). Source reference: 05aPaxmann.pdf

_Note: Full agenda and retrospective available via Handelsblatt Live

[25] Auge-Dickhut, Stefanie (BEI St. Gallen). Handelsblatt Conference 2025 (on AI strategy and adoption). Source reference: 03Aude-Dickhut.pdf

_Note: Full agenda and retrospective available via Handelsblatt Live